Soft Inquiry vs Hard Inquiry Explained in 2026

By Subhash Rukade | Updated May 27, 2026

Why Credit Inquiries Matter More in 2026

Millions of Americans are searching for soft inquiry vs hard inquiry explained because credit checks now play a bigger role in borrowing decisions, loan approvals, and financial planning in 2026.

Today, lenders carefully analyze credit reports before approving:

- Mortgage applications

- Credit cards

- Auto loans

- Business financing

- Personal loans

Because borrowing costs remain high across America, financially disciplined consumers now focus heavily on understanding how credit inquiries actually affect credit scores.

However, many beginners still misunderstand the difference between soft inquiries and hard inquiries.

Some Americans incorrectly believe:

- All credit checks hurt scores

- Pre-approvals damage credit heavily

- Monitoring scores lowers credit health

- Hard inquiries stay forever

Unfortunately, these myths often create:

- Unnecessary financial stress

- Poor borrowing decisions

- Lower score confidence

- Fear of credit monitoring

Financially disciplined Americans usually prioritize:

- Smarter loan shopping

- Responsible borrowing habits

- Credit monitoring awareness

- Long-term financial discipline

Consumers wanting deeper understanding of smarter credit card systems also continue learning through:

Ultimate Credit Card Guide 2026: Best Cards, Rewards & Smart Usage Tips.

The good news is Americans may still protect and improve credit scores once they understand how soft inquiries and hard inquiries actually work.

In this beginner-friendly 2026 guide, we’ll explain the difference between soft inquiries and hard inquiries, how credit checks affect borrowing decisions, common inquiry mistakes consumers make, and the smarter financial habits disciplined borrowers use to maintain stronger long-term credit health.

How Credit Inquiries Actually Work in 2026

Understanding soft inquiry vs hard inquiry explained starts with learning how modern credit inquiry systems actually work in America.

In 2026, lenders and financial institutions carefully review credit reports before approving:

- Credit cards

- Mortgage loans

- Car financing

- Business loans

- Personal credit lines

Unfortunately, many Americans still misunderstand how credit inquiries influence credit score systems.

This confusion often creates unnecessary financial fear and poor borrowing decisions.

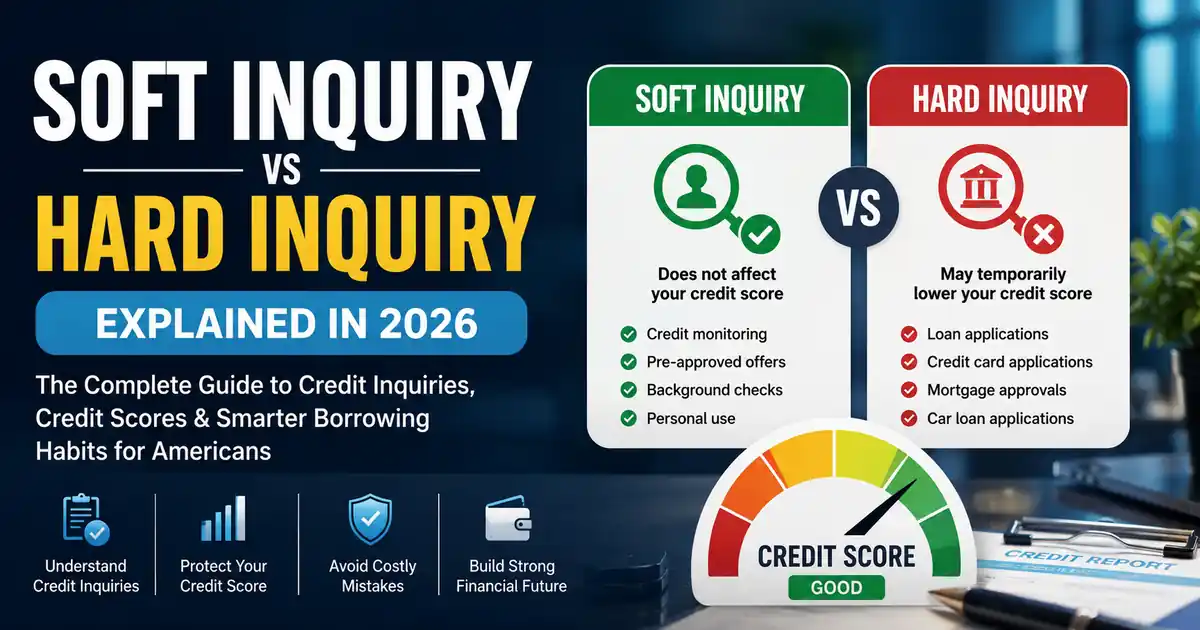

What Is a Soft Inquiry?

A soft inquiry usually happens when credit information is reviewed for educational or pre-approval purposes without a formal lending decision.

Soft inquiries commonly happen during:

- Personal credit score checks

- Background screening

- Pre-approved credit offers

- Credit monitoring services

- Employer verification checks

Most soft inquiries usually do not reduce credit scores.

Financially disciplined Americans often monitor scores regularly because stronger awareness helps identify:

- Fraud risks

- Utilization problems

- Credit report errors

- Suspicious account activity

What Is a Hard Inquiry?

A hard inquiry usually occurs when lenders review credit reports during formal borrowing applications.

Hard inquiries commonly happen during:

- Credit card applications

- Mortgage applications

- Car loan approvals

- Personal loan requests

- Business financing reviews

Hard inquiries may temporarily reduce credit scores because lenders view multiple borrowing requests as higher financial risk.

However, financially disciplined Americans understand occasional hard inquiries are usually normal during responsible financial planning.

Credit Bureaus Track Inquiry Activity Carefully

Major U.S. credit bureaus monitor inquiry activity to evaluate:

- Borrowing behavior

- Financial stability

- Repayment discipline

- Lending risk levels

Too many hard inquiries within short periods may signal:

- Financial stress

- Aggressive borrowing

- Debt accumulation risks

- Unstable financial management

| Soft Inquiry | Hard Inquiry | Main Difference |

|---|---|---|

| Personal credit checks | Loan applications | Formal lending review |

| Usually no score impact | May lower scores temporarily | Risk evaluation difference |

| Pre-approval systems | Final application review | Borrowing commitment level |

| Background screening | Mortgage applications | Lender involvement |

| Credit monitoring activity | New credit requests | Financial risk analysis |

Many Americans also continue strengthening broader financial preparedness through:

How Americans Are Protecting Their Money During a Recession in 2026.

Consumers planning stronger long-term financial stability also continue learning through:

Retirement Healthcare Planning Strategies.

Understanding how soft inquiries and hard inquiries actually work may help Americans avoid financial myths while maintaining healthier long-term borrowing discipline in 2026.

Major Differences Between Soft Inquiries and Hard Inquiries in 2026

Even in 2026, many Americans still confuse soft inquiries and hard inquiries because both involve credit report activity.

However, understanding soft inquiry vs hard inquiry explained may help consumers protect credit scores while making smarter borrowing decisions.

Financially disciplined Americans usually understand one important fact:

Not every credit check damages credit scores.

Soft Inquiries Usually Do Not Hurt Credit Scores

Soft inquiries are generally considered low-risk financial reviews because they usually happen without formal borrowing commitments.

Soft inquiries commonly occur during:

- Personal credit score monitoring

- Pre-approved offers

- Employer background checks

- Insurance quote reviews

- Credit monitoring services

Most soft inquiries usually:

- Do not reduce credit scores

- Remain invisible to lenders

- Improve financial awareness

- Help identify fraud risks

Financially disciplined Americans often monitor scores regularly because stronger awareness helps maintain healthier long-term financial stability.

Hard Inquiries May Temporarily Lower Credit Scores

Hard inquiries happen when lenders review credit reports during formal borrowing applications.

Hard inquiries usually occur during:

- Mortgage applications

- Credit card approvals

- Car financing requests

- Personal loan applications

- Business financing reviews

Hard inquiries may temporarily lower credit scores because lenders interpret multiple borrowing requests as possible financial risk.

However, financially disciplined borrowers understand occasional hard inquiries are usually normal during responsible financial planning.

Loan Shopping Windows Help Protect Credit Scores

Many Americans worry shopping for mortgages or auto loans may destroy credit scores.

Fortunately, modern scoring systems often group similar loan inquiries within short periods into:

- Single mortgage shopping events

- Single auto loan shopping periods

- Lower risk lending evaluations

This helps financially disciplined borrowers compare loan offers responsibly without causing unnecessary score damage.

Too Many Hard Inquiries May Signal Financial Stress

Multiple hard inquiries within short periods may sometimes indicate:

- Aggressive borrowing behavior

- Financial instability

- Debt accumulation risks

- Poor repayment planning

Financially disciplined Americans usually avoid:

- Unnecessary loan applications

- Emotional borrowing decisions

- Frequent credit card approvals

- Risky financial behavior

Many investors also continue strengthening passive income systems through:

Top Dividend Stocks USA 2026.

| Financial Activity | Inquiry Type | Credit Score Impact |

|---|---|---|

| Checking personal score | Soft inquiry | Usually no impact |

| Pre-approved credit offer | Soft inquiry | Usually no impact |

| Mortgage application | Hard inquiry | Temporary score reduction |

| Auto loan application | Hard inquiry | Possible short-term impact |

| Credit monitoring service | Soft inquiry | Usually no impact |

Recommended Credit Monitoring Resource

Many Americans continue tracking inquiry activity and monitoring financial health through:

Experian Credit Monitoring

.

Financially successful Americans now understand stronger credit scores are usually protected through smarter borrowing habits, responsible loan shopping, and better financial awareness — not fear of every credit inquiry.

Real-World Example and Common Credit Inquiry Mistakes

Even after understanding soft inquiry vs hard inquiry explained, many Americans still make financial mistakes because they misunderstand how credit inquiries affect long-term borrowing health.

Credit inquiries themselves are not automatically dangerous.

However, poor borrowing habits often create:

- Lower credit score stability

- Higher interest costs

- Loan approval concerns

- Financial stress

Real-World Example: Daniel From Texas

Daniel, a 34-year-old small business owner from Texas, wanted to improve his financial profile before applying for a mortgage in 2026.

At first, Daniel misunderstood how hard inquiries worked.

He believed:

- Applying for multiple credit cards was harmless

- Every lender offered the best rates automatically

- Loan shopping had no score impact

- Credit monitoring damaged scores

Because his financial discipline became inconsistent:

- Multiple hard inquiries appeared quickly

- His credit score temporarily dropped

- Lenders viewed borrowing activity cautiously

- Mortgage preparation became stressful

Daniel later realized smarter borrowing habits mattered far more than chasing unnecessary approvals.

He eventually improved his financial behavior by:

- Reducing unnecessary applications

- Using pre-approval systems carefully

- Monitoring scores regularly

- Applying only for essential financing

As his borrowing discipline improved, his credit score gradually stabilized again.

Too Many Hard Inquiries May Signal Financial Risk

Many Americans apply for multiple credit cards or loans emotionally during financial stress or promotional offers.

Unfortunately, excessive hard inquiries may sometimes signal:

- Debt accumulation risks

- Financial instability

- Aggressive borrowing behavior

- Poor repayment planning

Financially disciplined Americans usually prioritize:

- Smarter loan comparisons

- Planned borrowing systems

- Controlled credit applications

- Long-term financial stability

Ignoring Credit Monitoring Creates Problems

Some Americans avoid checking credit reports because they incorrectly fear soft inquiries will damage scores.

However, avoiding credit monitoring may create:

- Undetected fraud risks

- Missed reporting errors

- Identity theft exposure

- Delayed financial awareness

Financially disciplined consumers usually review reports regularly to maintain healthier long-term borrowing stability.

| Common Inquiry Mistake | Financial Consequence | Smarter Alternative |

|---|---|---|

| Too many loan applications | Multiple hard inquiries | Planned loan shopping |

| Emotional borrowing | Debt accumulation risks | Budget discipline |

| Avoiding credit monitoring | Fraud exposure | Regular score reviews |

| Frequent card applications | Temporary score reduction | Selective borrowing |

| Ignoring inquiry history | Lender risk concerns | Financial awareness |

Consumers wanting deeper understanding of smarter credit systems also continue learning through:

Ultimate Credit Card Guide 2026: Best Cards, Rewards & Smart Usage Tips.

Many Americans also continue improving long-term investing discipline through:

How to Build a Dividend Portfolio.

Understanding how inquiry mistakes develop remains extremely important because financially disciplined habits may help Americans maintain stronger credit stability while avoiding unnecessary borrowing risks in 2026.

Practical Strategies Americans Use to Protect Credit Scores in 2026

After understanding soft inquiry vs hard inquiry explained, the next important step is learning how financially disciplined Americans protect credit scores while maintaining healthier borrowing habits.

In 2026, many consumers successfully maintain stronger credit stability by focusing on:

- Smarter loan shopping

- Controlled borrowing behavior

- Lower utilization ratios

- Budget-focused repayment systems

- Long-term financial discipline

1. Smart Loan Shopping Helps Reduce Hard Inquiry Risks

Financially disciplined Americans usually avoid applying for multiple loans randomly.

Instead, they:

- Research lenders carefully

- Use pre-approval tools first

- Compare rates strategically

- Apply only when necessary

This helps consumers:

- Reduce unnecessary hard inquiries

- Protect score stability

- Improve lender confidence

- Maintain healthier borrowing behavior

Responsible loan shopping remains one of the smartest long-term financial habits in modern America.

2. Lower Utilization Ratios Improve Financial Stability

Many financially disciplined Americans now prioritize:

- Below 30% utilization

- Single-digit utilization when possible

- Smaller revolving balances

- Consistent repayment systems

Lower utilization often signals:

- Better financial discipline

- Lower lending risk

- Healthier repayment behavior

- Long-term financial stability

Many successful borrowers now make multiple monthly payments instead of waiting for statement deadlines.

3. Budget Planning Helps Americans Avoid Risky Borrowing

Many consumers struggle financially because emotional spending habits lead to unnecessary borrowing decisions.

Financially disciplined Americans usually divide income into:

- Essential expenses

- Debt repayment

- Emergency savings

- Investment contributions

- Lifestyle spending

This helps consumers:

- Reduce financial stress

- Prevent emotional borrowing

- Improve repayment consistency

- Maintain healthier credit stability

Many investors also continue strengthening wealth protection systems through:

Gold Investment Strategies USA.

Recommended Budgeting and Credit Tracking Resource

Many Americans continue improving financial discipline and monitoring inquiry activity through:

Credit Karma Credit Monitoring

.

Financially successful Americans now understand stronger credit stability usually develops through smarter borrowing systems, lower utilization habits, and responsible long-term financial planning.

These practical financial strategies may help Americans protect credit scores while avoiding unnecessary hard inquiry risks in 2026.

Future Credit Monitoring Trends and AI Banking Systems in 2026

The financial industry is evolving rapidly, and many experts believe the systems connected to soft inquiry vs hard inquiry explained will continue changing dramatically during the next few years.

In 2026, banks and financial technology companies are increasingly using:

- Artificial intelligence

- Real-time inquiry monitoring

- Personalized lending analysis

- Virtual banking systems

- Advanced fraud prevention tools

Because financial awareness continues growing across America, financially disciplined consumers now prioritize both credit score optimization and long-term financial security.

AI Credit Monitoring Is Becoming More Advanced

Modern banking apps can now automatically analyze:

- Borrowing behavior

- Inquiry activity

- Repayment consistency

- Utilization patterns

- Financial risk signals

Many AI systems help Americans:

- Track hard inquiries instantly

- Monitor suspicious account activity

- Reduce emotional borrowing

- Improve financial awareness

- Protect long-term score stability

These tools are becoming extremely popular because many consumers want smarter ways to protect credit scores while avoiding dangerous borrowing habits.

Real-Time Inquiry Alerts Improve Financial Awareness

Some financial institutions now provide instant alerts whenever:

- Hard inquiries appear

- New accounts open

- Loan applications occur

- Suspicious borrowing activity develops

This helps consumers:

- Detect fraud faster

- Improve account security

- Monitor borrowing activity

- Protect financial stability

Financially disciplined Americans increasingly rely on real-time monitoring systems to avoid unexpected financial problems.

Virtual Banking Systems Continue Expanding

Virtual banking systems and digital lending platforms continue growing rapidly across America in 2026.

Modern digital systems now offer:

- Pre-approval tools

- AI lending analysis

- Automated budgeting systems

- Digital fraud protection

- Virtual card management

These tools help consumers maintain stronger financial discipline while reducing unnecessary borrowing risks.

| Future Credit Trend | Main Benefit | Potential Risk |

|---|---|---|

| AI credit monitoring | Smarter inquiry tracking | Technology dependence |

| Real-time inquiry alerts | Faster fraud detection | Too many notifications |

| Personalized lending analysis | Better borrowing decisions | Overspending temptation |

| Virtual banking systems | Improved convenience | Cybersecurity concerns |

| Automated budgeting tools | Healthier financial discipline | User overreliance |

Government Financial Education Resources Continue Expanding

Several official U.S. organizations now provide free financial education helping Americans better understand borrowing systems and long-term financial planning.

The Consumer Financial Protection Bureau provides beginner-friendly financial education:

CFPB.gov.

The Federal Trade Commission helps consumers stay aware of fraud and scam risks:

FTC Consumer Protection.

The U.S. Securities and Exchange Commission also provides long-term investing education:

SEC.gov.

Recommended Personal Finance Book

Many financially disciplined Americans continue improving money habits and long-term financial thinking through:

The Psychology of Money

.

Technology may continue changing borrowing systems rapidly.

However, financially successful Americans now understand smarter loan management, controlled borrowing behavior, and responsible financial discipline will always remain the most important factors for maintaining stronger long-term credit stability in 2026 and beyond.

Frequently Asked Questions About Soft Inquiry vs Hard Inquiry in 2026

Do Soft Inquiries Hurt Credit Scores?

No. Most soft inquiries usually do not reduce credit scores because they are commonly used for educational reviews, pre-approval systems, and personal monitoring.

Soft inquiries often happen during:

- Checking personal credit scores

- Pre-approved credit offers

- Background verification

- Credit monitoring services

Financially disciplined Americans often review credit reports regularly because stronger awareness helps maintain healthier financial stability.

How Long Do Hard Inquiries Stay on Credit Reports?

Hard inquiries may remain visible on credit reports for up to two years.

However, their score impact usually becomes smaller over time.

Financially disciplined borrowers usually focus on:

- Responsible loan applications

- Controlled borrowing behavior

- Long-term repayment consistency

- Lower utilization ratios

Healthy financial habits often matter far more than occasional hard inquiries.

How Many Hard Inquiries Are Considered Safe?

There is no exact universal number.

However, multiple hard inquiries within short periods may sometimes signal:

- Aggressive borrowing behavior

- Financial instability

- Debt accumulation risks

- Poor repayment planning

Financially disciplined Americans usually apply only for essential credit products instead of chasing unnecessary approvals.

Do Pre-Approval Offers Hurt Credit Scores?

Most pre-approval systems usually use soft inquiries instead of hard inquiries.

This means pre-approval checks often:

- Do not lower credit scores

- Improve financial awareness

- Help compare loan options

- Support smarter borrowing decisions

However, final loan applications usually trigger hard inquiries during official lender reviews.

How Fast Can Credit Scores Recover After Hard Inquiries?

Credit recovery speed depends on:

- Repayment consistency

- Utilization management

- Long-term borrowing discipline

- Overall financial stability

Many Americans gradually improve score stability through:

- Controlled borrowing systems

- Lower revolving balances

- Automatic payment setups

- Responsible financial planning

Final Thoughts on Soft Inquiry vs Hard Inquiry Explained

Understanding soft inquiry vs hard inquiry explained has become increasingly important because millions of Americans now depend on stronger credit profiles for mortgages, loans, investing opportunities, and long-term financial flexibility.

When consumers misunderstand how credit inquiries work, they often create:

- Unnecessary financial stress

- Poor borrowing decisions

- Lower score confidence

- Long-term financial instability

However, financially successful Americans now understand stronger credit stability usually develops through:

- Smarter borrowing systems

- Controlled loan applications

- Responsible repayment habits

- Lower utilization ratios

- Long-term financial discipline

Consumers wanting deeper understanding of smarter credit card systems also continue learning through:

Ultimate Credit Card Guide 2026: Best Cards, Rewards & Smart Usage Tips.

Many Americans also continue improving long-term investing discipline through:

How to Build a Dividend Portfolio.

The biggest lesson Americans should remember is simple:

Smarter borrowing discipline and financial awareness usually protect credit scores far better than avoiding every credit inquiry out of fear.

Responsible financial habits today may help Americans build stronger confidence, lower stress, and healthier long-term financial stability in 2026 and beyond.

Join Our Financial Freedom Community

Want smarter investing strategies, credit score improvement tips, beginner-friendly credit card guides, and long-term financial planning ideas in 2026?

Subscribe to Finance Investment and receive easy-to-understand financial education designed for Americans building stronger financial futures.

Leave a Reply